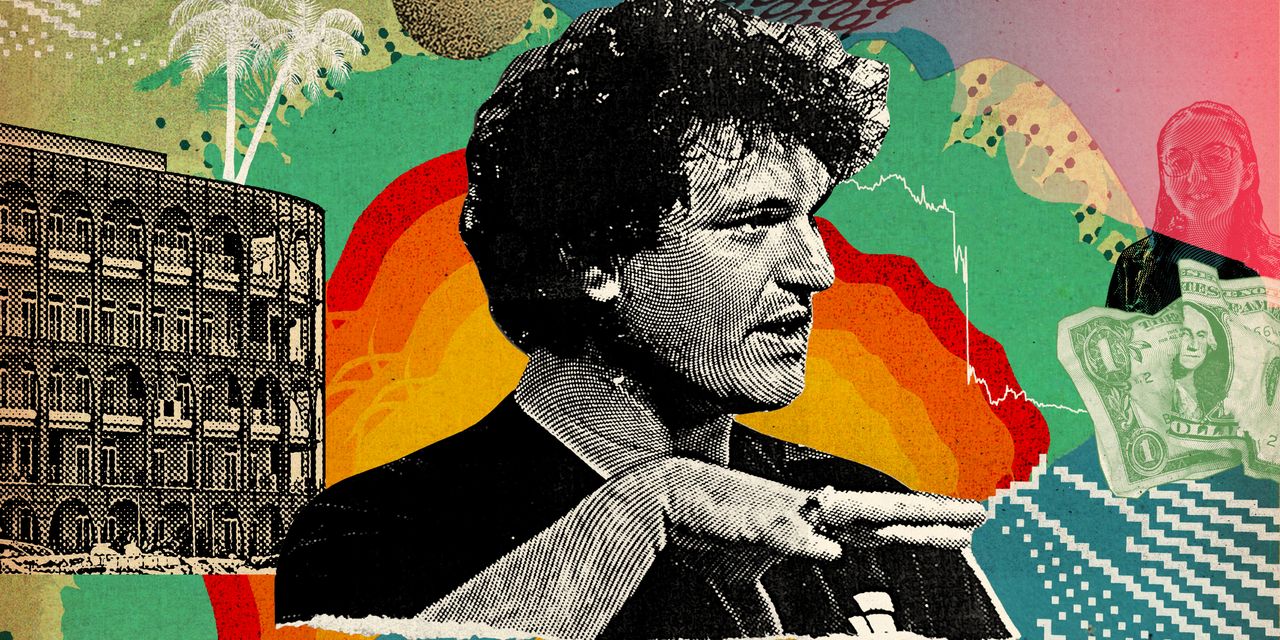

NASSAU, Bahamas—Sam Bankman-Fried’s $32 billion crypto-trading empire collapsed in an incandescent bankruptcy last week, prompting irate customers, crypto acolytes and Silicon Valley bigwigs to ask how something that seemed so promising could have imploded so fast.

The emerging picture suggests FTX wasn’t simply felled by a rival, or undone by a bad trade or the relentless fall this year in the value of cryptocurrencies. Instead, it had long been a chaotic mess. From its earliest days, the firm was an unruly agglomeration of corporate entities, customer assets and Mr. Bankman-Fried himself, according to court papers, company balance sheets shown to bankers and interviews with employees and investors. No one could say exactly what belonged to whom. Prosecutors are now investigating its collapse.

24World Media does not take any responsibility of the information you see on this page. The content this page contains is from independent third-party content provider. If you have any concerns regarding the content, please free to write us here: contact@24worldmedia.com

SWAMPSCOTT — Music, gardens, art, and community will come together on Sunday, July 5, from 1 to 3 p.m....

SAUGUS — Timothy Gregory, 55, of Boston, and Derek Matarazzo, 38, of Charlestown, were arraigned...

The sky over Red Rock Park and King’s Beach will light up with fireworks Friday night, thanks in part...

NAHANT — A farmer’s market-style food program is helping feed local veterans in Nahant with fresh...

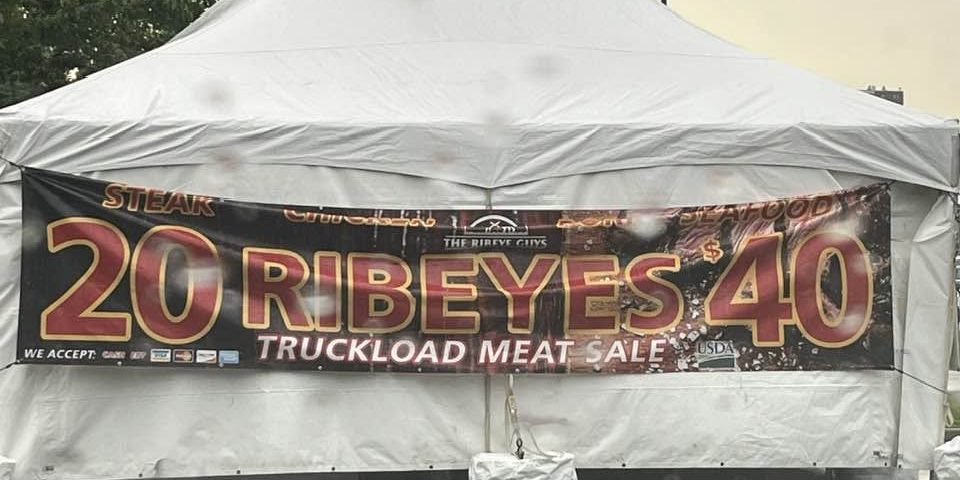

Swampscott probes meat tent Erin Hickey July 1, 2026 by Erin Hickey SWAMPSCOTT — A pop-up meat tent...

The City and the People’s Budget Coalition have announced a partnership with Northeast Justice Center,...

Southold issues stop-work order at controversial 6,000-hen egg farm

Youth sailing program rides into Lynn

Youth Summer Series ready to run

Marblehead Seasiders climbing every day

10 Things to Do in July

Greenport Rotary donates $1K to support young readers at Floyd Memorial Library

Today’s page 1: 7-1-26

How to beat the heat

Police Logs: June 29, 2026

Walsh named American Hospital president

Winning big at Gannon – Itemlive

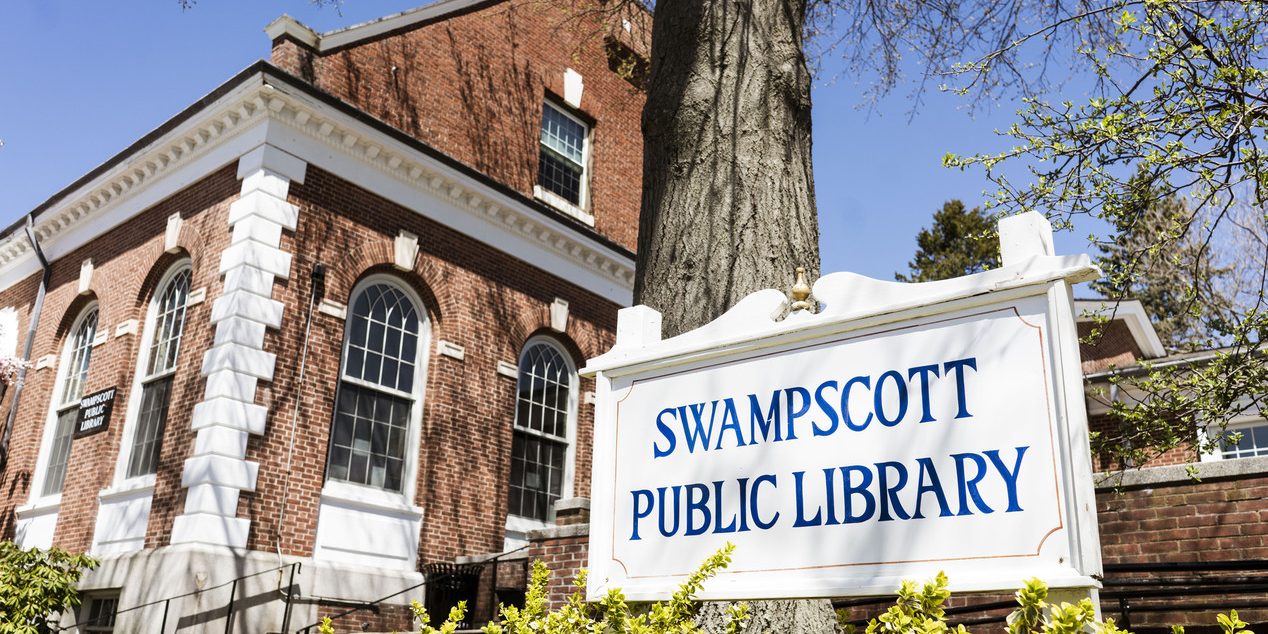

Swampscott library checks the books